- IN THE NEWS X

- It’s time to clear your advance tax liability

- Seniors need to submit Forms 12BBA, 15G, 15H to save on TDS: Experts

- How investing in 54EC bonds can help you save tax on long-term gains

- New income tax forms are out for new assessment year 2022-23. Find out which one you should use

- New ITR forms need income disclosure from foreign retirement a/cs

- Why is March 31 an important date for taxpayers? Find out

- Not filed ITR yet? Face penalty or even jail term, say analysts

- March 15 Is The Last Date To Pay Advance Tax: Time To Clear Your Liability

- It's time to deduct TDS if rent exceeds Rs 50,000, say analysts

- Clarification on capital gains tax on early redemption of Sovereign Gold Bonds is required – Here’s why

- Second amendment to LLP Rules will ease procedural burden: Experts

- Three Things To Keep In Mind Before Investing In RBI’s Sovereign Gold Bonds

- Tackle low liquidity in sovereign gold bonds by laddering, say analysts

- CBDT, tax tools make e-filing of I-T returns simpler

Senior and Super Senior Citizens may choose the Old Tax Regime or the New Tax Regime, i.e., under Tax Slabs for AY 2022-23

Written by Gagandeep Arora - Printed on - Date - 14th Dec 2022

For income tax purposes, a resident is deemed to be a senior citizen if they had been 60

or older but under 80, whereas an individual resident who was 80 years of age or older

at any point in the previous financial year is referred to as a super senior citizen.

Senior and Super Senior Citizens may choose the Old Tax Regime or the New Tax Regime,

i.e., under Tax Slabs for AY 2022-23. There are several exemptions and deductions, such

as 80C, 80D, 80TTB, and HRA, that are not available to taxpayers who choose tax

concessions rates under the New Tax Regime when compared to the old tax regime. What tax

brackets and income tax deductions are available to senior and super senior citizens?

Let’s find out from our tax experts.

Senior citizens are defined as an individual who is 60 years of age or above but less

than 80 years of age. Anybody who is 80 years old or above is considered to be a super

senior citizen as per Income Tax Act. This bifurcation is done to give additional tax

benefits for people reaching 80 years.

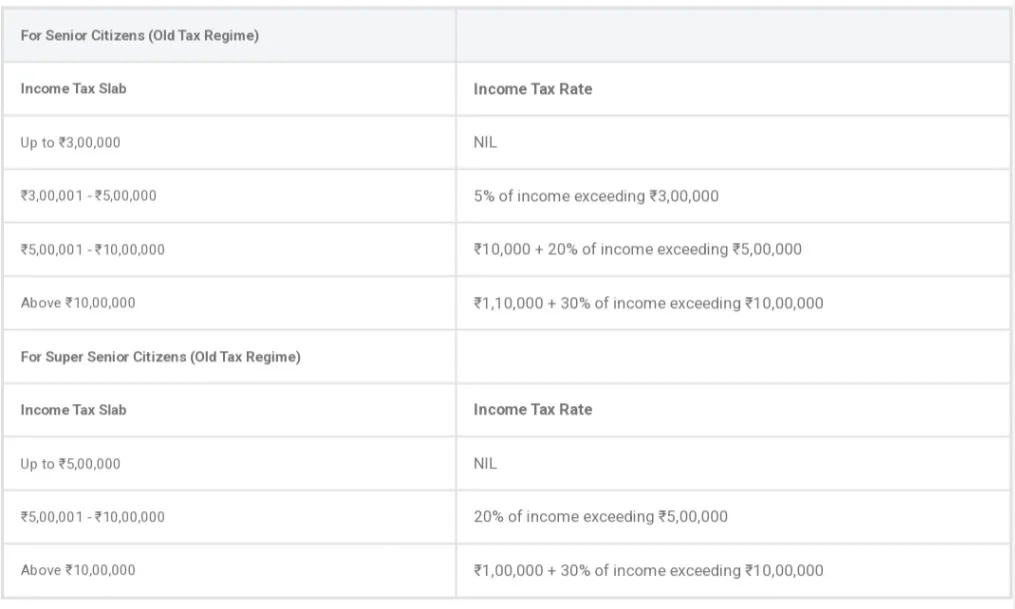

One should note that under the old tax regime, senior citizens get a basic exemption of

3,00,000 i.e., an income earned up to 3,00,000 is tax free. On the other hand, for super

senior citizens, this basic exemption limit is raised to 5,00,000.

You may check the income tax slabs for senior and super senior citizens under old tax

regime in the table below: –

It is important to note that a Rebate of Rs. 10,000 u/s 87A is applicable for senior

citizens if their total income is not more than 5 lacs. Therefore, effectively senior

citizens will not have to pay any tax if their income is up to 5 lacs.

However, if the income crosses the mark of 5 lacs, then they will have to pay tax on the

entire income exceeding 3 lacs.

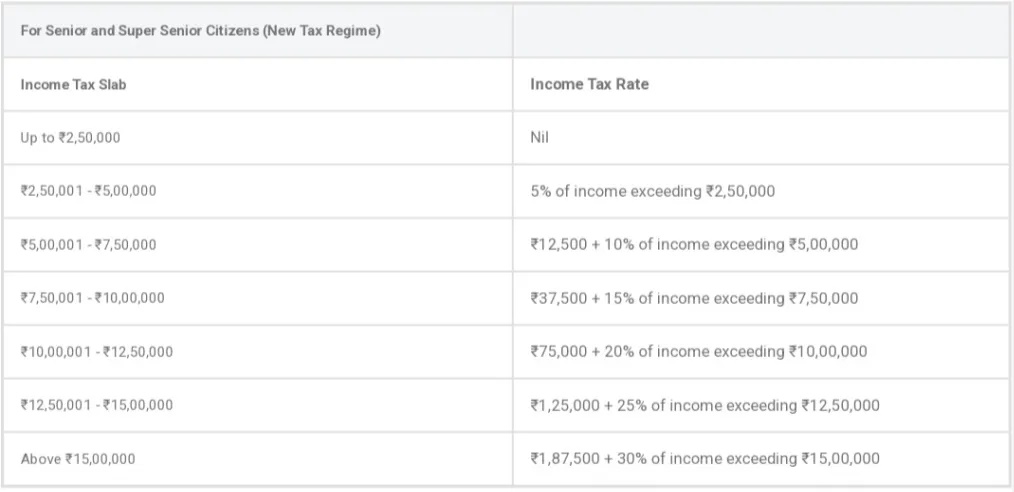

If opting for the new tax regime, no additional exemption is available for senior and

super senior citizens. Under the new tax regime, there is only one category of slabs

which is applicable for all individuals with no categorization of senior or super senior

citizens. Here, the basic exemption limit is lower at 2.5 lacs.

Opting for a new tax regime means lower tax rates but with a disadvantage of not being

able to claim most of the deductions and exemptions like 80C, 80D, HRA, 80TTB etc.

In the following table, you will find the income tax slabs for senior and super senior

citizens under the new tax regime: –

Individuals should note that rebate of up to 12,500 u/s 87A is available in the new tax

regime if the income is not more than 5 lacs.

Taxpayers should keep in mind that they will be liable to pay surcharge if their taxable

income exceeds 50 lacs. Rate of surcharge increases with increase in level of income

ranging from 10%-37% of income tax payable.

Additionally, health & education cess at 4% will also be levied on the amount of income

tax plus surcharge.

Total Income

Income tax rates (Senior Citizen) under Old

Tax Regime

Total Income

Income Tax rates (Irrespective of the taxpayer’s age)

under New Tax Regime

Upto Rs. 3,00,000*

Nil

Upto Rs. 2,50,000*

Nil

Rs. 3,00,001 – Rs. 5,00,000

5.2% [tax rate 5% plus health and education cess 4% thereon] (Effective

Rate is Nil after availing rebate u/s 87A**) of income exceeding Rs.

3,00,000

Rs. 2,50,001 – Rs. 5,00,000

5.2% [tax rate 5% plus health and education cess 4% thereon] (Effective

Rate is Nil after availing rebate u/s 87A**) of income exceeding Rs.

2,50,000

Rs. 5,00,001 – Rs. 7,50,000

20.80% [tax rate 20% plus health and education cess 4% thereon] of

income exceeding Rs. 5,00,000

Rs. 5,00,001 – Rs. 7,50,000

10.40% [tax rate 10% plus health and education cess 4% thereon] of

income exceeding Rs. 5,00,000

Rs. 7,50,001 – Rs. 10,00,000

20.80% [tax rate 20% plus health and education cess 4% thereon] of

income exceeding Rs. 5,00,000

Rs. 7,50,001 – Rs. 10,00,000

15.60% [tax rate 15% plus health and education cess 4% thereon] of

income exceeding Rs. 7,50,000

Rs. 10,00,001 – Rs. 12,50,000

31.20% [tax rate 30% plus health and education cess 4% thereon] of

income exceeding Rs. 10,00,000

Rs. 10,00,001 – Rs. 12,50,000

20.80% [tax rate 20% plus health and education cess 4% thereon] of

income exceeding Rs. 10,00,000

Rs. 12,50,001 – Rs. 15,00,000

31.20% [tax rate 30% plus health and education cess 4% thereon] of

income exceeding Rs. 12,50,000

Rs. 12,50,001 – Rs. 15,00,000

26.00% [tax rate 25% plus health and education cess 4% thereon] of

income exceeding Rs. 12,50,000

Rs. 15,00,001 – Rs. 50,00,000

31.20% [tax rate 30% plus health and education cess 4% thereon] of

income exceeding Rs. 15,00,000

Rs. 15,00,001 – Rs. 50,00,000

31.20% [tax rate 30% plus health and education cess 4% thereon] of

income exceeding Rs. 15,00,000

Rs. 50,00,001# – Rs. 1,00,00,000

34.32% [(tax rate 30% plus surcharge 10% thereon) plus health and

education cess 4% thereon] of income exceeding Rs. 50,00,000

Rs. 50,00,001# – Rs. 1,00,00,000

34.32% [(tax rate 30% plus surcharge 10% thereon) plus health and

education cess 4% thereon] of income exceeding Rs. 50,00,000

Rs. 1,00,00,001# – Rs. 2,00,00,000

35.88% [(tax rate 30% plus surcharge 15% thereon) plus health and

education cess 4% thereon] of income exceeding Rs. 1,00,00,000

Rs. 1,00,00,001# – Rs. 2,00,00,000

35.88% [(tax rate 30% plus surcharge 15% thereon) plus health and

education cess 4% thereon] of income exceeding Rs. 1,00,00,000

Rs. 2,00,00,001# – Rs. 5,00,00,000

39% [(tax rate 30% plus surcharge 25%^ thereon) plus health and

education cess 4% thereon] of income exceeding Rs. 2,00,00,000

Rs. 2,00,00,001# – Rs. 5,00,00,000

39% [(tax rate 30% plus surcharge 25%^ thereon) plus health and

education cess 4% thereon] of income exceeding Rs. 2,00,00,000

Above 5,00,00,000#

5,00,00,001 and above 42.744% [(tax rate 30% plus surcharge 37%^

thereon) plus health and education cess 4% thereon] of income exceeding

Rs. 5,00,00,000

Above 5,00,00,000#

42.744% [(tax rate 30% plus surcharge 37%^ thereon) plus health and

education cess 4% thereon] of income exceeding Rs.5,00,00,000

Note(i)*:– Any resident senior citizen whose age is more than 60 years but less than

or equal to 80 years has a basic exemption limit of Rs. 3,00,000 as mentioned in the above

table. Further, any resident taxpayer who is a super senior citizen whose age is more than

80 years has a basic exemption limit of Rs. 5,00,000 instead of Rs. 3,00,000.

Note(ii)#:– Marginal relief is available to ensure that the additional income tax

payable, including surcharge of 10%, 15%, 25% or 37% on the excess of income over Rs.

50,00,000, Rs. 1,00,00,000, Rs. 2,00,00,000 or Rs. 5,00,00,000 as the case may be, is

limited to the amount by which the income is more than Rs. 50,00,000, Rs. 1,00,00,000, Rs.

2,00,00,000 or Rs. 5,00,00,000 as the case may be. However, no marginal relief shall be

available in respect of the health and education cess.

Note(iii)^:- Maximum rate of surcharge on tax payable on income chargeable to

special tax rate under section 111A, 112A, 112, 115AD(1)(b) and dividend income shall be

15%.

Note(iv)**:- Rebate u/s 87A is applicable in case of new tax regime and needs to be

availed for the amount of tax payable or Rs. 12,500, whichever is lesser, resulting in NIL

tax liability provided the taxpayers total income is upto Rs. 5,00,000.

Note(v):- Special income would be chargeable @ special tax rates mentioned in Section

111A, 112, 112A, etc.

Further, any taxpayer availing the concessional tax regime / new tax regime would not be

eligible to claim the following deductions (which can be claimed in old tax regime):

· 10(13A) – House Rent Allowance

· 10(5) – Leave travel Concession

· 10(14) – Special allowance detailed in Rule 2BB (such as children education

allowance, hostel allowance, etc. other than transport allowance, travel allowance, daily

allowance).

· 10(17) – Allowances received by MP, member of state legislature, etc.

· 10(32) – Clubbing benefit of Rs. 1500 per minor child

· 10AA – Deduction for SEZ unit

· Section 16 – Standard Deduction of Rs. 50000, Entertainment Allowance,

Professional Tax

· 24(b) – Interest on borrowed loan for a Self Occupied property or Vacant Property

u/s 23(2)

· 32(1)(iia) – Additional Depreciation

· 32AD – Investment Allowance for investment in Andhra Pradesh / Telangana / Bihar /

West Bengal

· 33AB – Tea / Coffee / Rubber Development

· 33ABA – Site Restoration Fund

· 35(2AA) – Deduction for Payment to National Laboratory or University or IIT

· 35AD – Deduction in respect of specified business

· 35CCC – Expenditure on agricultural extension project

· 57(iia)- Family pension

· Any provision of chapter VI – A – section 80C, 80D etc. However, Section 80CCD(2)

(employer contribution on account of employee in a notified pension scheme) can be claimed.